What is the Difference Between a Manufactured Home and a Modular Home?

That’s a question we get asked frequently, and for good reason. The terminology surrounding “factory-built” homes (there’s another term!) can be confusing. Both a manufactured home and a modular home are built in a controlled factory setting. Both are built in boxes or modules with plumbing, electrical, and mechanical installed in the factory. Both have similar inspection processes. Both are transported to a site and installed. There are even companies that build both manufactured and modular homes.

But there are some key differences you need to be aware of that could impact financing, appraised value, durability, and even safety in some cases!

Codes and standards

Manufactured homes are built to a federal standard governed by the U.S. Department of Housing and Urban Development (HUD). This is a pre-emptive standard, meaning all fifty states must allow these types of homes. However, many states do not allow HUD homes in certain residential zones due to local aesthetic and land-use preferences. Manufactured homes can be installed on a permanent or non-permanent foundation and will be affixed to a steel chassis to allow for durability during transportation and installation.

A modular home is built to the International Residential Codes (IRC), which are the same state and local building codes as conventional site-built homes. As such, there is less national standardization during the review and approval process, which can add time on the front end.

Safety

A manufactured home requires smoke alarms, egress windows, and limited fire separations. A modular home includes more stringent fire-resistant construction and fire separation requirements. Additionally, a manufactured home is designed to meet one of three national zones defined by HUD for wind and thermal efficiency and two zones for seismic loads.

Manufactured homes in Wind Zone III are designed to withstand sustained wind speeds of 110 mph, which is equivalent to a peak gust of approximately 130 mph. This zone is mostly in coastal locations along the coastlines of states like Florida, Louisiana, and Texas, where hurricanes are more frequent. By contrast, a modular home built to the IRC in the same regions must be able to withstand winds of 140 -180 mph, depending on the location.

HUD standards provide prescriptive structural designs that do not always require site-specific engineering. This allows HUD homes to follow simplified national guidelines, which can be advantageous for standard product lines but may limit architectural variation.

Modular homes must account for local wind, snow, and seismic loads, which vary widely and are addressed using detailed engineering or prescriptive code tables. IRC modular homes are engineered based on site-specific needs (e.g., soil, wind, snow loads).

HUD framing typically uses two-by-four wood framing (or sometimes steel framing) with simplified framing details. Modular IRC Homes requires two-by-six framing for exterior walls in cold climates (per energy code), with stricter bracing and framing member rules.

Financing, Appraisal, and Equity

Given that a modular home is built to all the same codes and standards as a conventionally constructed site-built home, it stands to reason that conventional financing options are similar. Occasionally, a lender will not understand the difference between a manufactured and a modular home and needs to be further educated on the differences.

While there have been steps taken to improve the financing options for manufactured homes, including FHA, VA, and in some cases conventional loans, lenders are still hesitant to provide loans to these types of homes, particularly if they are not considered real property.

In some cases, chattel loans can finance the home itself, but not the land it sits on. They are typically used when the manufactured home is not considered real property (meaning it is not on a permanent foundation and/or the land is not owned by the homeowner).

One of the big concerns about manufactured homes is the long-term equity gained by the homeowner. For many families, particularly those in the lower to middle income brackets, their home is the largest asset and a key driver of wealth accumulation.

Most appraisers will treat manufactured and modular homes differently when assessing value. While modular homes are treated similarly to site-built homes and often used as comps, manufactured homes are typically compared to other similar properties.

Most appraisers will treat manufactured and modular homes differently when assessing value. While modular homes are treated similarly to site-built homes and often used as comps, manufactured homes are typically compared to other similar properties.

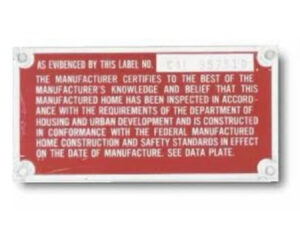

It can come as quite a shock to the home seller or buyer if they believe the home is modular and the lender and appraiser determine it is a manufactured home. A manufactured HUD home will have a steel chassis connected as part of its foundation system. It will also bear a red insignia from HUD attesting that the home meets the federal standards.

Summary

A manufactured home is a great option for a family seeking a quality, affordable home. With improved financing options and greater “curb appeal” designs, these manufactured homes look almost indistinguishable from their modular home counterparts. But that is where the risk comes in for you as the home buyer.

We hope this article provides you with some basic information about the key differences between manufactured and modular homes, or at least equips you with the right questions to ask your builder.